Operations on Futures

Last updated on April 10, 2021

|

1) The conditions 2) The required margin 3) value date 4) Contracts of the FTSE MIB Futures, Mini FTSE MIB, FTSE 100 Mini 5) The liquidation 6) The risks 7) stop order 8) "trading'' environment's Customization |

The commissions (per contract) could be either easy or dynamic.

Easy

CME: $ 6 - CME Fx $ 3 (micro $ 1) - CME CBOT: $ 8

FTSE MIB, FDAX: 6 euros

MINI, EUROSTOXX50, FBUND: 4 euros

DYNAMIC

MINI, ESTX50, FBUND: from 8 to 1.5 euros

FTSE MIB, FDAX: from 9 to 2.5 euros

CME: from 9 to $ 2.5 (not applicable to the CBOT segment and to the micro contracts of $ 1)

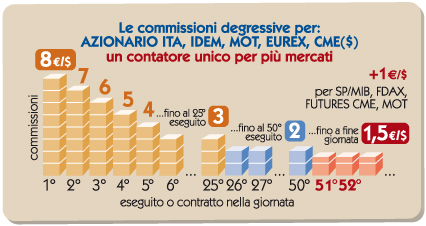

The counting of the degressive reduction is the same between

FTSE MIB / MINI FTSE MIB / MTA / SEDEX / EUREX / CME :

for the first order of the day on the stock market, SEDEX or FTSE MIB / MINI FTSE MIB the initial commission plan is applied (8 Euros if it's on shares, SEDEX, or MINI; and 9 euros if it's on the FTSE MIB, and 9 euros if it's on CME); for the second order, even if it's carried out on a different instrument, Second commission plan is applied (7 euros if it's on the Shares stock exchange, SEDEX, MINI; and 8 euros if it's on FTSE MIB and 8 dollars if it's on the CME). And so on so forth ... up to € 3 per share, SEDEX, MINI, 4 euros for the FTSE MIB and $ 4 for the CME starting from 6th transaction to 25th; from 26th executed trade to the 50th the commission will still decrease up to € 2 on the MTA, SEDEX, and MINI FTSE MIB and on the MINI FTSE 100, FBUND, FESX, € 3 on the FTSE MIB and the FDAX, and $ 3 for the CME Futures; from the 51st to the end of the day one reaches the minimum commission, with further discount of € 0.50 / $ (and thus € 1.5, € 2.5 and $ 2.5, respectively).

REQUIRED MARGINS: Please check out table here

MARGIN ADJUSTMENT DEADLINE : h 10.15

ORDER VALIDITY : 1 day; for IDEM, and also multi-day validity for EUREX

STOP ORDER VALIDITY: 1 day

VALUE DATE: next day

TRADING HOURS : Please see the main table

2) The required margin

The required margin varies according to the futures' contract and is returned at the time of the position closing.

For the Italian futures, the margin is a percentage of the nominal value of the contract, whereas the Eurex and CME the margin for each contract is flat.

The aforementioned table shows all the margins required by Directa.

Let's suppose that at the end of the stock market session a customer has an open position on a futures' contract:

- If the position was open during the day, the difference between the end-of-day closing price and the opening price of the position is calculated

- If the position was already opened at the beginning of the session, the difference between the end-of-day closing price and the previous closing reference price is calculated.

If the calculated difference is positive, that's, the future's price has increased, then the LONG positions are in GAIN while the SHORT positions are in LOSS ; and vice versa if the difference is negative.

Let's see what happens to the customer's position in the 4 possible scenarios:

POSITIVE DIFFERENCE

1) LONG GAIN = the customer collects the difference between the GAIN and the increase in the payable margin compared to the day before

2) SHORT LOSS = the customer pays the sum between the LOSS and the increase in the payable margin compared to the day before

NEGATIVE DIFFERENCE

3) LONG LOSS = the customer pays the difference between the LOSS and the margin reduction

4) SHORT GAIN = the customer collects the sum between the GAIN and the margin reduction

NOTE: If the margin requirement is fixed, as the case for Eurex and CME, the customer's position will simply be increased by the GAIN or reduced by the LOSS depending on the case, without margining adjustment.

3) value date

Regarding the availability and the value date, you should note that the transactions on the equities' stock market are regulated according to two or three days deadline, depending on the markets, whereas the futures' value date is the next day; hence, the sale of a stock share does not provide liquidity to cover the margin / loss with regard to an open futures' position, while the closing of a futures' contract provides liquidity to purchase stock shares.

But Directa has already provided since November 2006, the allocation of a fund of its own to draw on to cover this and other value date displacements or delays with an interest-free loan for the benefit of its customers, for whom directa provides also, in any case, the availability calculation in real time: and therefore simplifying greatly the operation, because the customer can always easily know their purchasing power, both for equities and the derivatives alike, without further checks.

4) FTSE MIB Futures and the Mini FTSE MIB contracts

The Mini FTSE MIB and FTSE MIB Futures are equivalent contracts, with the same maturity and expiration date, according to the proportion 1 FTSE MIB Future = 5 Mini FTSE MIB. The CCG allows to exchange one FTSE MIB Future with 5 Mini FTSE MIB, if so desired.

An investor can, for instance, buy 1 FTSE MIB Future, sell 1 Mini FTSE MIB and so find himself long for 4 Mini FTSE MIB. If he sells one FTSE MIB Future at this point, he would be short for 1 Mini FTSE MIB. Directa allows to freely combine purchases and sales of FTSE MIB Futures and the Mini FTSE MIB, by maintaining always, at constant maturity date, a one single counting for both the two derivative securities. So, if the investor has purchased 7 Mini FTSE MIB in the following market phases, he will be shown "1 FTSE MIB Futures + 2 Mini FTSE MIB" and will be able to operate on both the instruments according to the price conveniences.

Let' us suppose, for example, that the investor is short for 3 FTSE MIBs and, depending on the market developments, decides not only to close the short position, but also to take a long position by performing the so-called stop and reverse : in this case, he might find to be more suitable to buying one FTSE MIB Future, instead of buying a certain number of Mini FTSE MIBs, to take advantage, of course, of the minor effect of the commissions on a single operation, which would transform the short positions of the 3 Mini FTSE MIBs into 2 long positions.

'5) The liquidation

'

In the event of unfavorable changes in the trends, the futures' price goes down in the long position, and goes up, in case of a short , so that the investor must cover the margin requirements (and / or the loss ); and given the short time available (until 10:10 am of the following day), he could usually do so in the following ways:

- by obtaining liquidity from other positions held with the Broker, for instance, by the selling off some shares

- by partially liquidating the derivatives' position.

If, for example, an investor was short for a FTSE MIB and, being forced, for an increase of the trends, to adjust the margins, did not have the necessary cash amount on the account, he may partially liquidate the position by buying 1 Mini FTSE MIB ( and thus transforming it into a short position of 4 Mini FTSE MIB); and in case of FDAX or mini Nasdaq 100, he could close a contract.

Lastly, it will be Directa that, one hour past the opening of the market, with the investor having yet to cover the margins, will eventually carry out any operations it deems most appropriate to reduce or equalize the position.

6) The risks

What are the differences between a future and a covered warrant ?

They are both defined as derivative securities and both provide a leverage effect, but in reality, we're talking about very different financial instruments.

The CW provides the "benefit" of never putting at risk anything more than the invested capital: those who purchase a CW for 10,000 euros will "at worst" lose 10,000 Euros, but will never get themselves into debt.

By contrast, with the futures, the losses to be covered could even exceed the initially invested capital.

The CWs often have cash flow problems and lack of transparency in the price formation: since that the price trends will most likely depend, to a large extent, on the management of the security as handled by the Market Maker , the trading on the CWs is often resolved in a "duel" with it self.

As for the more liquid futures, the counterparties are numerous, the spread very low, the price changes very fast, opportunities for scalping are then more frequent, but also more difficult to grasp.

Who has developed a good experience in the cw operation, by passing over to the futures' trading will find himself in a new territory, where many of the techniques used on the cws are inapplicable.

7) stop order

Also on the futures, the market offers, both in purchases and in sales, the stop order function. The order details are placed on directa's online trading platforms exactly the same way and parameters as for the stop orders on the stock market. These are orders sent immediately to the market, that remain pending ONLY UNTIL END OF THE DAY, or until the expected price condition occurs, if this happens, a normal purchase or sales order is carried out.

Imagine, for example, to be long on a futures' contract and the market price is 21,000, and to place sell at the limit price of 21,100 by placing simultaneously an stop order at the trigger price of 20,950 : if the Market goes up, and the order is executed at 21,100, the stop order is not cancelled; namely, if we "forget" to withdraw it, in the event of subsequent drop up to 20,950 the order will be executed and we will find ourselves short of one future's contract.

The introduction of the futures' markets on the OCO provides an additional tool to overcome this inconvenience.

NB: We would like to remind here two peculiarities:

- The stop orders on the IDEM market can be can be placed at any time, even when the market is closed, but will get into active trading only during the continuous trading session.

- When operating on the Eurex market it's impossible to specify a limit price.

8) "trading'' environment's Customization

You can enter the futures into the basic platform tables by using the menu item Options then derivatives' section.

with regard to the "FTSE MIB" table, note that it's simply enough to add either the FTSE MIB or the mini FTSE MIB of a particular deadline to make the other element of the "couple" show up.